HomePro still growing & a REIT in the future

‎Several companies (in fact all!) have been releasing their earnings over the past week, one that caught my eye was HomePro (HMPRO) for a few reasons:

- Same store sales still grew @ 6.5% in 2Q14 and +5.3% for 2H14

- They will continue to expand throughout Thailand & Malaysia

- An upcoming dividend & potential REIT

To expand on each point further…

SSSG

Management said was driven by a recovery in demand for home products and robust TV sales ahead of the FIFA World Cup, this despite every other retailer exhibiting either negative growth rates and only +1-2% SSSG, so perhaps the debt bingeing that every economist/investor has been warning about doesn’t affect HMPRO’s customer segment. Although going forward for 2H14 (yes a bit short term looking) I wouldn’t be surprised to see SSSG decrease slightly to 4-5% just purely because there isn’t the world cup effect.

Continued expansion

They are still planning to expand throughout Thailand with five HomePro stores in Thailand and its first branch (their first international one) in Malaysia in 2H14. A key point that management made was the in Thailand all of the expansion would be in first-tier cities, as demand in second and third-tier cities still remain weak. In 2015 they still plan to open 6-8 HomePro stores and 4 Mega Home outlets in Thailand and a second branch in Malaysia by 2016. Now I wouldn’t be surprised if Malaysia & Mega Home are a continued drag for their earnings because a) operations in Malaysia should take 4-5 years to break even on a corporate level and at least 4 stores would be required to achieve operating leverage. b) Mega Home should only be profitable by 2015 because they’ll have the usual opening losses, pre-operating expenses, marketing etc etc that all are associated with opening a new store format.

Dividend & Asset Spin-off

With everything happening the company still plans to pay a dividend in 2H14 based upon its 1H14 earnings, now I would expect for them to pay a stock dividend rather than cash because HMPRO has an annual capex plan of THB 8-9 bn and looking at their balance sheet I wouldn’t be surprised to see them try and raise equity via the stock dividend scheme. Now for its Asset spin-off, management did mention that it plans to sell its Hua Hin Market Village to a REIT (either their own or anothers) next year, officially that property is valued at THB 4-5 bn, thus HMPRO should yield a net gain of THB 1.6-2.0 bn.

I’m going to try and comment more on companies news and events going forward, although I still refuse to give investment recommendations as everyone’s risk/return, time horizon, objectives are different.

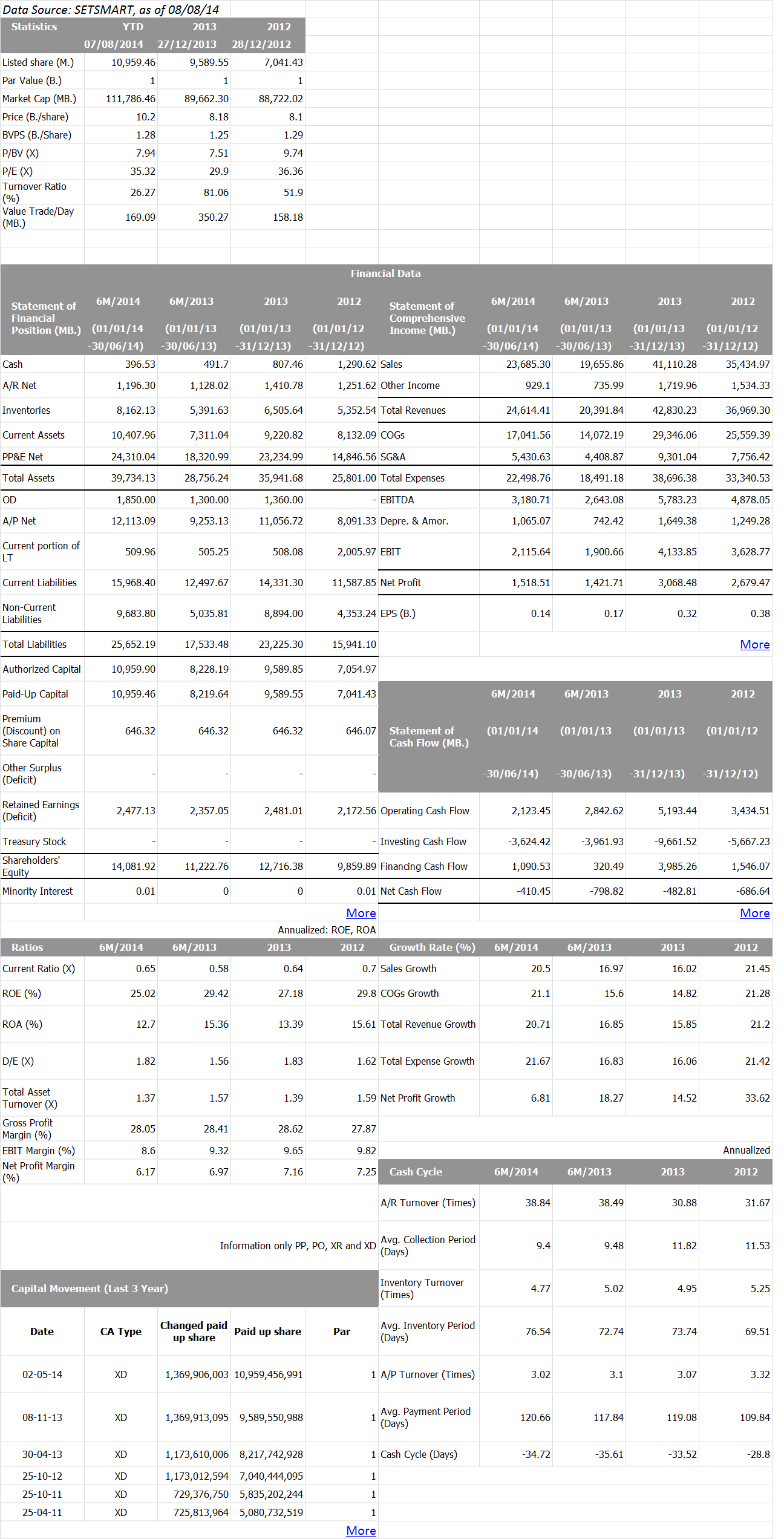

Financials Snapshot